What Amazon Can't Buy

How a $700 million company in Mexico built the distribution network and moat $13 billion of Amazon and Mercado Libre investment could not.

Believe it or not, there is a consumer goods company posting 67% gross margins, 27% return on capital employed, and 83% free cash flow conversion. It has paid massive dividends for 25 consecutive quarters without interruption, through a leveraged acquisition, a consumer slowdown, and two years of currency depreciation. Its EBITDA has compounded at roughly 25% annually for seven years.

P&G posts 51% gross margins. Unilever posts 44%. Both have been in their core markets for over a century. Both have global supply chains, world-class logistics, and every structural advantage a consumer goods company can accumulate.

This company, with 67% margins, sells kitchen organizers and bathroom storage products through women in Mexican neighborhoods most investors have never visited.

The explanation requires understanding where this company operates, as well as who it works through; and it starts with a concept from physics. And right now, one week after a transformative acquisition closed at 3.1x EBITDA that the market has not priced in, the founder's family is buying stock; for the first time in the company’s multi-decade history.

Resonance

In 1831, a British infantry regiment marched across the Broughton Suspension Bridge in Manchester. While marching in step, the bridge started to vibrate. Then it swung. Finally, it collapsed into the River below.

Unlike what many thought, the bridge did not fall because the soldiers were heavy. It fell because their synchronized footsteps matched the bridge’s natural frequency.

In Physics, the equation governing such frequencies is:

F(t) = F₀ cos(ωt)

where ω is the driving frequency(the soldiers) and ω₀ is the system’s natural frequency(the bridge). When ω equals ω₀, the response amplitude(the result) grows independent of the magnitude of the input force. When they diverge, energy dissipates regardless of how large the force is. In simpler words, you can apply enormous power; but at the wrong frequency produce almost nothing.

Every physical system has a natural frequency determined by its structural parameters. The only way to drive the system efficiently is to match it. Amazon has invested $3 billion in Mexico since 2015. Mercado Libre has invested $10.5 billion between 2020 and 2025. P&G has operated in Mexico for decades. None of them have effectively captured the market this company serves. I argue that it isn’t a matter of effort or capital, but a matter of frequency. These MNO’s operate at a fundamentally different frequency than the Mexican economy, allowing this company to quietly penetrate the market. That company is Betterware de Mexico.

The System Nobody Designed For

Mexico has a structural feature that most analysts read past.

55% of Mexican women work in informal conditions, without a contract, without health services, and without employment benefits. Women’s workforce participation stands at 46% versus 77% for men. At the current rate, closing that gap would take 119 years. Informal workers earned an average of $252 per month in 2023, versus $371 for formal workers. In the first half of 2025 alone, over 1.13 million people joined informal employment, the highest first-semester increase ever recorded excluding the pandemic, while formal employment contracted by 278,470 jobs simultaneously.

These women live in places called “colonias populares”: semi-formal neighborhoods built without formal planning. Most run without standardized addresses, as streets are either named informally or not at all. Transactions happen largely in cash, between people who know each other personally. Moreover, Childcare is expensive, fixed-hour employment requires leaving home, and formal employment stands a large geographic distance away.

The structural parameters define the resonant frequency: things like cash transactions, informal addresses, community trust as the primary medium of exchange, flexible hours, and products priced for households earning just $250 to $400 per month, make all the difference.

These parameters cannot be changed by applying more force.

What Betterware de Mexico Actually Does

Betterware de Mexico sells various home organization products. Think accessories for a kitchen, bedroom, or bathroom, as well as technology. Products range from a mere 20 Pesos to 1700, distributed across 9 product catalogs per year.

The products aren’t generic. Betterware’s works with more than 12 universities and uses anthropologists to develop products specifically for such “colonias populares” households. They design stackable food containers designed for a typical apartment kitchen, shoe racks for the narrow entryway of a working-class home, bedroom storage for small rooms shared by multiple people, and much more. These do not exist in the same form anywhere else at the same price.

But the real magic comes in the distribution model.

Betterware has no employees selling its products! Rather, every person who touches a product after it leaves the warehouse is an independent contractor, organized in two tiers:

The first tier is the distributor. Betterware has roughly 63,000 of them. A distributor is a small business owner managing a geographic territory in a colonia popular they know well. They order products from Betterware at wholesale, paying upfront. For Betterware, revenue is recognized at that moment. From then on, the distributor owns the inventory and the risk, and thus, they usually come in with a network of contractors called associates. On average every distributor has 20 of them, and it is their responsibility to train and motivate them, as well as earn the spread between what they pay Betterware and what the associate pays.

There are roughly 1.13 million associates.

The associate sells to neighbors through personal trust relationships, delivers personally, extends informal credit, and collects cash at catalog retail price. Subsequently, they earn the spread between what they pay the distributor and what the end consumer pays.

Keep this in mind for the following sections: approximately 80% of Betterware’s distributor and associate base is women.

Here is the full picture. Betterware sources one of their products, like a kitchen organizer, from China for roughly 30 pesos landed. It sells to the distributor at 90 pesos. At that point, Betterware’s job and risk is over, earning themselves roughly 67% gross margins. The distributor sells to the associate at MXN 110, and finally, the associate sells to the end consumer at MXN 140. Betterware never touches the end consumer transaction.

This is why Betterware’s margin profile is so much better than other retailers. They don’tt pay for salesforce salaries, retail shelf placement, trade spend, advertising to end consumers, or last-mile logistics! All of those costs happen two layers below its P&L, funded entirely by distributor and associate margin. The income statement consequence is 67% gross margins in what looks like a consumer products business. That number is the direct mathematical output of having externalized the entire commercial cost structure of a consumer goods company to 1.19 million independent contractors who bear it voluntarily in exchange for their own margin spread. Betterware operates at ω₀. P&G and Amazon are driving at ω₁.

The Deal That Built the Moat

This begs the question; what’s in it for the distributors and associates? Well here is where the story gets interesting. Betterware made deals with these women starting 30 years ago, and those deals are structurally permanent. Put yourself in the shoes of a lower-class, hard-working, Mexican woman.

She has two children. Her husband works construction on variable wages. She has a secondary school education and no formal employment history. She cannot take a fixed-hours job because childcare would consume most of what she earned. And unfortunately, the formal economy around her has nothing compatible with her actual life.

In comes Betterware, offering her a chance at a career; one where she can build her own “business”... on her own terms.

She first joins as an associate, at zero cost. There’s no startup fee and no minimum catalog purchase required upfront. As per her own schedule and confidence, she orders products from distributors and sells them to her neighbours. The Working capital requirement is essentially zero, and she can work while her children are in school or asleep. A moderately active associate generates 3000-5000 pesos in monthly sales and earns 750 to 1,500 pesos per month in margin. In a household typically earning MXN 8,000 to 12,000, that is a 10 to 20% income increase with zero commute and zero childcare conflict.

Over the years, she accumulates a customer base that automatically reorders every catalog cycle. Neighbours call her first when a product launches. That customer base is not transferable to any other platform. It exists because of who she is and how long she has been there. Walking away means walking away from years of accumulated social capital and a recurring income stream no other institution could have helped her build. As she moves from associate to distributor, she earns from the activity of 15 to 20 women beneath her. That leverage does not exist in any formal job available to her. That is the moat.

Mark Twain once said: ““History Doesn’t Repeat Itself, but It Often Rhymes”. Costco built one of the most durable retail businesses in American history not primarily by optimizing for its own margins, but by offering a deal good enough that every participant in the system had a genuine reason to stay and make it work. Costco taught everyone that when you create enough value for the people your business depends on, they become the moat. Betterware found the same thing 30 years ago in Mexico’s colonias populares. By offering the only flexible income opportunity compatible with the actual lives of informally employed women, it unlocked 1.19 million people who built the distribution infrastructure themselves, using their own social capital, at their own cost, in exchange for their own margin.

Why Competitors Cannot Get In

The logic doesn’t lie! If this were really true, what happened with competitors who tried to penetrate the Mexican market?

Amazon serves approximately 14.2 million online shoppers in Mexico as of 2024, while Mexico has 130 million people. After 8 years and $3 billion, Amazon reaches just about 11% of the population, almost entirely in formal urban centers.

Mercado Libre’s same-day delivery, despite $10.5 billion in Mexican investment, operates in a mere 25 cities across a country with thousands of municipalities.

Amazon and Mercado Libre require formal addresses, digital payments, and bank cards. Those things do not exist at scale in the colonias populares. More warehouses will not fix this. Amazon cannot give a woman in a colonia popular a business she owns, in her neighborhood, using her social capital, compatible with her children’s schedule, earning from other women’s selling activity. Even if Amazon tried to build a door-to-door network in informal neighborhoods, it would have to hire these women as employees, pay minimum wage, manage their hours, and bear their costs. That destroys the economics for these families.

Replicating Betterware’s distribution requires offering the same deal Betterware offered 30 years ago, and doing that requires a cost structure and time horizon no quarterly-reporting public company will accept. That is the truth!

P&G sells through formal retail. In a colonia popular where the nearest supermarket is a bus ride away, and a woman cannot leave home during school hours, the consumer never reaches the store. P&G has been in Mexico for decades, yet this market remains untouched.

The COVID Proof

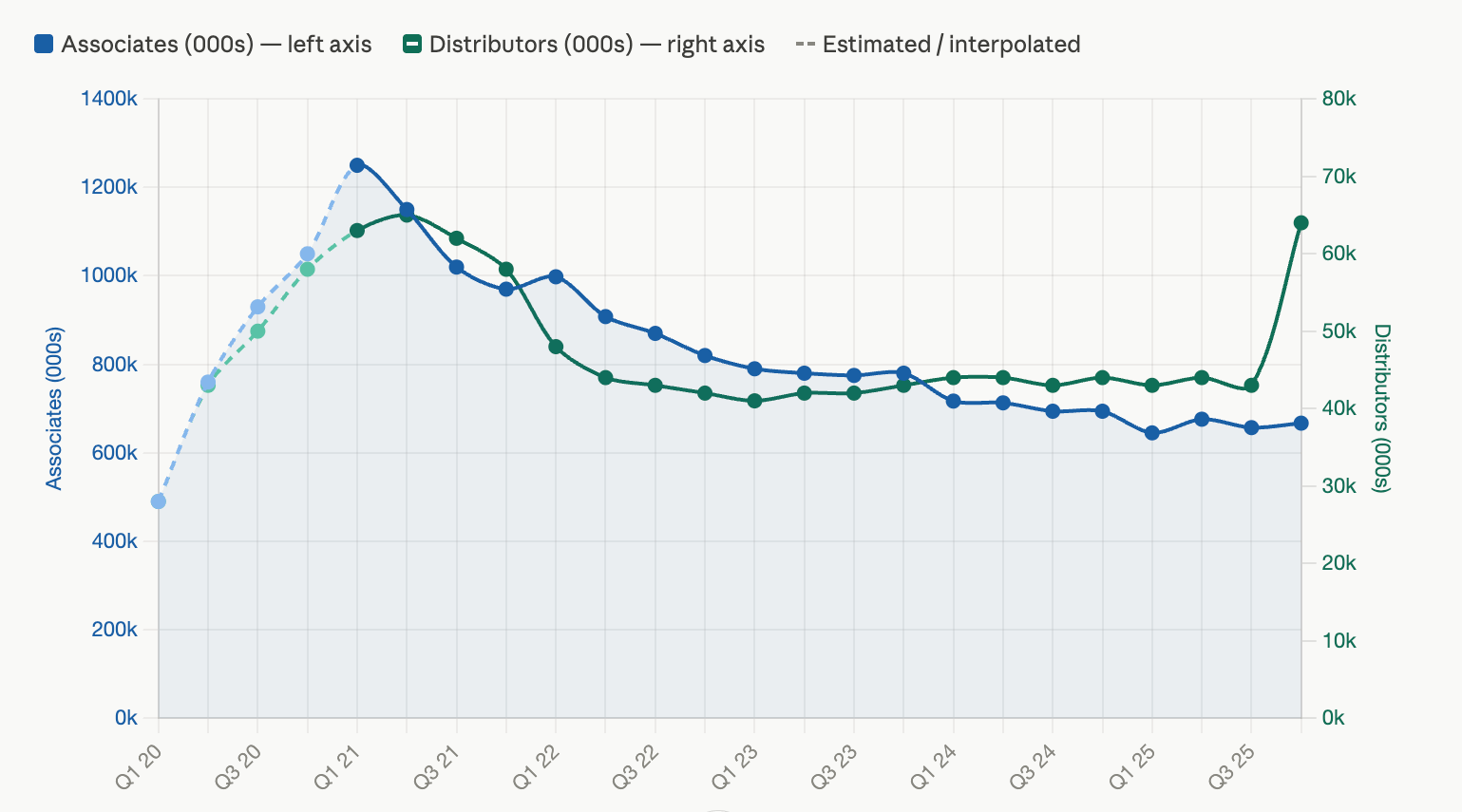

In 2020, during COVID, distributor and associate counts grew 108% and 94% respectively. Lower-class workers, stuck at home, all saw an opportunity for income. But that surge wasn’t durable. As the economy normalized in the subsequent years, the surge corrected back down, and revenue declined.

In reality, the participants who joined just because selling seemed effortless left, and the core participants remained. Behind the scenes, those women’s utilization rates held, orders increased, and Betterware eclipsed the Mexican market by 5x times during a consumer spending compression. In 2025, the associate base grew from Q1 to Q4 for the first time since COVID. The correction had concluded and growth went back to being funded by genuine value proposition.

With that context, the income statement looks completely different.

67% gross margins are the mathematical output of externalizing costs two layers below the P&L. 27% ROCE is nearly twice P&G’s 14 to 16% because growing commercially costs Betterware almost nothing. Free cash flow in 2025 was MXN 1.78 billion, up 24.6% year over year. EBITDA has compounded at roughly 25% annually from 2018 to 2025.

Net debt to EBITDA improved from 3.07x in 2022 to 1.56x by end of 2025. Three full turns of deleveraging in three years, entirely from operating cash flow, without cutting dividends or pausing expansion. MXN 700 million of debt repaid in 2025 alone. 25 consecutive quarterly dividends paid through currency devaluation, a leveraged acquisition, and a consumer slowdown simultaneously. The current yield is 7%! There were numerous instances in which they could have cut; yet they never did.

Jafra

Jafra now represents more than half of consolidated BeFra revenue, so explaining Jafra is imperative. In April 2022, Betterware acquired Jafra Cosmetics Mexico from Vorwerk Group. Jafra is Mexico’s direct selling beauty brand, selling fragrances, skincare, and color cosmetics through the same distributor-associate model. At acquisition, Jafra had been declining in revenue from 2019 to 2021. Within nine months, Jafra’s EBITDA reached MXN 272.4 million in Q3 2022, a 405% increase versus Q3 2021. By 2025, Jafra had gone from fourth to second in Mexico’s direct selling beauty channel, and ranked seventh in Mexico’s overall beauty market across all channels. In Q2 2025, Jafra Mexico grew revenue 10.9% while the overall Mexican beauty market grew just 5%.

The strategic importance here is the income ladder. The same distributor who sells Betterware kitchen organizers to a working-class household now has a Jafra beauty catalog when that same woman has slightly more discretionary income. The trust relationship built over years is monetized across two product lines without adding a single new relationship. While Betterware captures the household, Jafra captures the aspiration. As Mexico’s lower-class wage has risen 60% from 2022 to 2026, every peso of that incremental income flowing to households previously too constrained for discretionary spending becomes the new addressable market.

Tupperware

Luis Campos founded Betterware in Mexico in 1995. Before that, he served as President of Tupperware Americas from 1994 to 1999. He ultimately left to build what he believed was a better model at Betterware, and ran that model for 27 years. But in January 2026, he bought Tupperware’s entire Latin American operations out of bankruptcy at 3.1x EV/EBITDA.

The acquisition brings 200,000 trained salespeople, manufacturing plants in Mexico and Brazil, and a perpetual royalty-free brand license across all of Latin America. Tupperware LatAm generated $404 million in sales in 2022 before the global restructuring damaged it. The regional operations were profitable, it was just that the US parent wasn’t. Only the man who ran the regional business 27 years ago could acquire it because he fully understood what he was buying.

Tupperware sure is a delight for Betterware shareholders. The deal is immediately 40% EPS accretive, adding $81 million in annual EBITDA. At 10x trailing earnings, the Tupperware integration brings the total forward EPS multiple below 5! Not to mention, it adds Brazil, a 215 million person market, through a perpetual license.

BeFra now has three brands across three price tiers. Betterware for the working poor household. Jafra for the aspiring woman with discretionary income. Tupperware for the established household wanting premium branded kitchenware.

Not to mention, Befra isn’t limited to Mexico! Guatemala achieved 81% year-over-year revenue growth in Q4 2025. Ecuador surpassed 11,500 associates and 730 distributors at year-end with approximately 20% monthly revenue growth. Colombia launched in early 2026. The resonant frequency of Mexico’s informal economy is not unique to Mexico. The asset is in knowing and operating around it.

Valuation

All of this may establish Befra as a quality business, but what can this fruit going forward? BeFra reported cumulative FY2025 standalone EPS of $1.46. The Tupperware Latin America acquisition closed on June 2, 2026. On a pro forma basis including Tupperware and adjusted for acquisition financing costs, the combined FY2025 EPS would have been $2.11, representing 44.5% accretion.

Management guides 2026 revenue of MXN 14,800M to 15,400M with an EBITDA margin at or above 19%. Layer on organic growth in Betterware Mexico, Jafra’s continued market share gains, and early-stage expansion in Ecuador, Guatemala, and Colombia, and a reasonable forward EPS estimate for 2026 sits between $2.20 and $2.40 fully integrated. The stock currently trades at roughly $18.

At 10x earnings, consistent with a stable consumer business with moderate growth and currency risk, you get $22 to $24. That is where the stock trades if the market decides this is an ordinary business. At 14x, which is still a discount to the direct selling peer group and reflects the moat quality and brand ladder, you get $31 to $34. The dividend yield at current prices is approximately 6.7%, supported by 83% FCF conversion.

Risks

Currency. A meaningful portion of BeFra’s cost base is dollar-denominated, including China sourcing, while revenues are peso-denominated. Sustained peso depreciation compresses margins in dollar terms. This is permanent and recurring for every Mexican consumer business.

Controlling shareholders. The Campos family holds 54.2% of shares. The behavioral record argues in their favor. But minority shareholders have limited recourse if capital allocation priorities ever change. The disclosed material weakness in internal controls adds to this concern and should be tracked.

Integration execution. Jafra was absorbed cleanly. Tupperware is larger, has been through a global bankruptcy, and requires rebuilding distributor confidence in two large markets simultaneously. The 40% EPS accretion assumes the business stabilizes at current levels. If Tupperware Mexico’s revenue continues declining from its already-reduced $278 million base, the accretion math changes.

Conclusion

Luis Campos filed his first ever Form 3 with the SEC in March 2026, formally registering 19,597,829 ordinary shares. He has controlled this business for 30 years. He chose to make his ownership formally visible to US regulators for the first time simultaneously with the largest acquisition in the company’s history. And when he filed that Form 3, he bought shares. That was the first time in the stock’s history an insider purchased shares.

CEO Andrés Campos Chevallier purchased 10,000 shares in the open market at $16.81 in late April 2026. The people with the most complete information about what the Tupperware integration looks like on the inside, what the combined business will report, and where the Andean expansion is heading chose to buy at those prices.

Net debt is falling every quarter. The network is recovering. Two brand acquisitions have been absorbed and are growing. A third market is being entered through a perpetual license across an entire continent. It is only a matter of time before the market realizes the magic of the BeFra frequency.

Disclosure: I own shares in Betterware de Mexico (BWMX). This is not investment advice. All investments carry risk, including the total loss of capital. Do your own research. BWMX trades approximately $1.6 million in daily dollar volume.